Follow

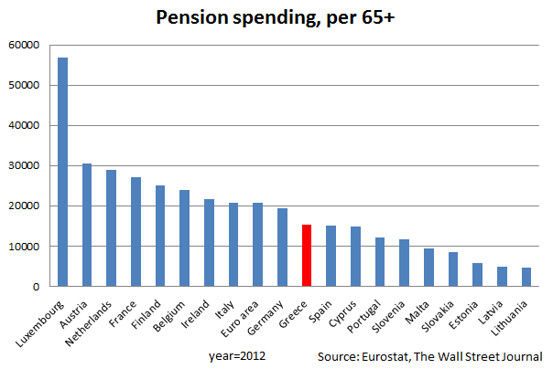

Follow Over a month ago I declared that the Grexit was a fait accompli. As soon as Chancellor Merkel publicly declared it was a possibility it was the only end game. Why? Because Greek debt is (and has been) unsustainable and there were ever only two finishes to the crisis: debt-relief or Grexit. The former would be a nice thing to do in a world devoid of political reality, but, for several reasons, it is never going to happen. First, the overwhelming sense of many important creditor nations (and several peripheral ones) was that Greek debt has been a result of Greek profligacy, and those countries can’t ask their tax payers to foot the bill for early Greek retirement. Second, even if these leaders could summon the “statesmanship” necessary to face down their own electorates, relieving Greek debt would create an incredible moral hazard for the other Eurozone debtor nations. If Greece is worthy of a debt write down than surely Ireland? or Portugal? or Spain? How could the ECB, IMF or European Governments refuse? 250 billion € can be managed (heck, Quantitative Easing has printed that much already), a trillion+ would be a bit more challenging. Finally, while it has certainly been bad in Greece, many parts of the EU (and EMU) are still far poorer. As this chart shows, per capita spending on pensions of the Baltic states is significantly less than half that in Greece. Other social spending shows similar relationships. Those invoking the “morality” of debt relief in Greece must think that the Greek elderly are somehow more deserving than their Lithuanian counterparts. The Slovakian finance minister recently made clear that nominal debt relief is a “red line”.

Over a month ago I declared that the Grexit was a fait accompli. As soon as Chancellor Merkel publicly declared it was a possibility it was the only end game. Why? Because Greek debt is (and has been) unsustainable and there were ever only two finishes to the crisis: debt-relief or Grexit. The former would be a nice thing to do in a world devoid of political reality, but, for several reasons, it is never going to happen. First, the overwhelming sense of many important creditor nations (and several peripheral ones) was that Greek debt has been a result of Greek profligacy, and those countries can’t ask their tax payers to foot the bill for early Greek retirement. Second, even if these leaders could summon the “statesmanship” necessary to face down their own electorates, relieving Greek debt would create an incredible moral hazard for the other Eurozone debtor nations. If Greece is worthy of a debt write down than surely Ireland? or Portugal? or Spain? How could the ECB, IMF or European Governments refuse? 250 billion € can be managed (heck, Quantitative Easing has printed that much already), a trillion+ would be a bit more challenging. Finally, while it has certainly been bad in Greece, many parts of the EU (and EMU) are still far poorer. As this chart shows, per capita spending on pensions of the Baltic states is significantly less than half that in Greece. Other social spending shows similar relationships. Those invoking the “morality” of debt relief in Greece must think that the Greek elderly are somehow more deserving than their Lithuanian counterparts. The Slovakian finance minister recently made clear that nominal debt relief is a “red line”.

{kind=link}

So Grexit it is. But Grexit need not be feared. The political argument against Grexit is weak, but the economic argument is weaker still. The EU is a political project. The EMU is primarily an economic project. Yes, it is not an optimal currency unit and has had its trials and tribulations, but that is largely because it contains states like Greece, who incidentally cooked their books to join. The exit of a suboptimal member out of a currency unit doesn’t make it weaker – it makes it stronger. Even if contagion spreads, which looks increasingly unlikely, and a few other suboptimal dominoes fall, say Portugal, this still isn’t fatal to the currency. An exchange rate is a price, based on supply and demand of and for a currency, which is driven, to a large extent, by the strength of the economy behind the currency. When an economy that is in the midst of a depression not seen since the 1930s leaves the fold how can markets do anything but cheer?

The refrain that the Euro is a “political project” is only partly true. Britain’s tensions with the EU have little to do with its maintenance of Sterling. Denmark is as much Europe as Belgium. Sweden has chosen an indefinite, de facto, opt out despite a legal obligation to join, and yet remains integral to the European project. Polish plumbers can live and work in France as easily as the Irish. These states all illustrate that EMU membership is NOT a necessary component of being part of the European political project. Many of the states out of the Euro are there because they do not feel the currency fits their macroeconomic goals. The Euro does not fit Greece’s macroeconomic goals and the prudent move is joining the outsiders. For most of the remaining “Eurozone 18” the Euro will continue to work, backed by the 4th, 6th, 8th, 14th and 17th largest economies in the world.

Grexit will be a painful adjustment for Greece, as outlined today in the WSJ, though probably no more than continued austerity and with at least some prospect of eventual recovery (and perhaps even readmission). Germany is right to (finally) call for humanitarian assistance which is vitally necessary as the Greeks rebuild the social safety nets while adjusting to the new Drachma reality. However, Grexit is not a boogeyman that will destroy the European project. Instead it is a sensible and effective separation that will ultimately leave both parties better off.